Units lead Melbourne price growth as apartments outperform houses: RPM

Melbourne’s apartment market entered 2026 with renewed momentum, but the recovery is uneven, policy-driven, and increasingly shaped by constrained supply.

According to the RPM Apartments & Townhomes Market Report (April 2026), apartments have begun to outperform detached housing on key metrics,yet that performance is occurring against a backdrop of falling approvals and a tightening development pipeline.

At the end of 2025, Melbourne unit values reached a three-year high of $656,500, recording quarterly growth of two per cent. That figure edged ahead of the 1.8 per cent growth recorded in the house market over the same period, marking a notable shift in relative performance. While modest in absolute terms, the outperformance is significant given the sustained dominance of houses through much of the previous cycle.

This shift has been driven in large part by policy. The federal government’s expanded five per cent Deposit Scheme has had a disproportionate impact on apartment demand, particularly in Melbourne where the $950,000 price cap captures a large share of medium- and high-density stock.

As RPM notes, the scheme “heavily favours medium and high-density dwellings,” effectively accelerating demand in the apartment sector.

The impact is most visible in buyer activity. Victoria recorded more than 43,000 new housing loans in Q4 2025, the highest quarterly volume since mid-2022 and one of the strongest results in over a decade. This lift was broad-based across all buyer types, with first home buyers, owner-occupiers and investors all returning to the market with greater confidence.

This surge in demand has flowed directly into apartment pricing, particularly in Melbourne’s middle and outer rings. Middle-ring unit values reached approximately $757,500, a four-year high, while outer-ring units climbed to a record $650,000. Quarterly growth of 2.9 per cent and 2.5 per cent respectively significantly outpaced both the inner ring (0.8 per cent) and the broader house market.

The divergence between apartments and houses is also being shaped by affordability. Detached housing remains out of reach for many buyers, pushing demand toward apartments as a more accessible entry point into well-located suburbs. This is particularly evident among first home buyers and downsizers, both of whom are increasingly prioritising location, amenity and lifestyle over land size.

At the same time, population growth continues to underpin demand. Victoria added more than 122,000 residents in the year to Q3 2025, with Melbourne attracting both overseas migrants and interstate movers, partly due to its relative affordability compared to other capitals.

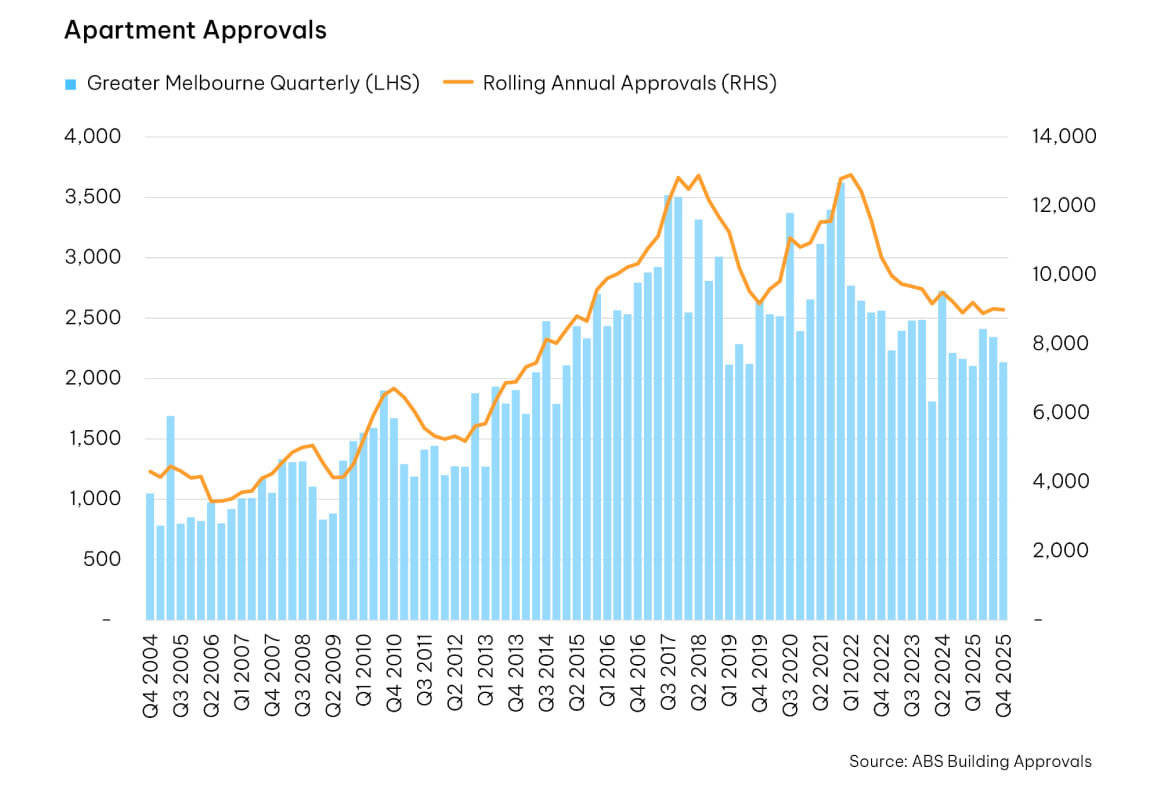

However, the most critical factor shaping the apartment market is not demand, it is supply.

Apartment approvals across Greater Melbourne have fallen sharply, signalling a constrained pipeline of future stock. In Q4 2025, just 2,339 apartments were approved, down 20 per cent on the previous quarter and 47 per cent lower than the same period a year earlier. On an annual basis, 11,066 apartment approvals were recorded, an improvement on the previous year, but still well below medium- and long-term averages.

This decline reflects a broader contraction cycle that has been underway since 2020. As RPM notes, “apartment approvals appear to be sliding back into a downward trend,” with developers increasingly focused on launching and completing existing projects rather than initiating new ones.

The reasons are well understood. Construction costs have risen more than 20 per cent since 2021, driven largely by labour shortages and material price escalation. At the same time, financing conditions have tightened, with lenders requiring higher contingencies and taking a more cautious approach to risk. Combined with recent interest rate rises, these factors have made feasibility more challenging, particularly for higher-density projects.

This dynamic is creating a disconnect in the market. Demand for apartments—particularly at the more affordable end—is strengthening, while the pipeline of new supply is weakening. In the short term, this may limit the number of new projects coming to market. Over the medium term, however, it is likely to support price resilience and potentially further outperformance relative to houses.

There are some signs of policy-driven supply response. The introduction of Victoria’s Mid-Rise Code, which streamlines approvals for four- to six-storey developments, is expected to improve delivery in well-serviced middle-ring locations. However, this is unlikely to materially offset the broader decline in apartment approvals in the near term.

Despite the positive momentum at the end of 2025, the outlook for 2026 has become more complex. Two interest rate rises early in the year have already impacted consumer confidence, while broader cost pressures, particularly energy and fuel, are feeding through to construction and development costs.

“Victoria’s built form market ended 2025 on a high, but early 2026 rate rises quickly reversed the momentum,” RPM notes.

The implication is that while apartments are currently outperforming houses, the trajectory of that outperformance will depend on how these competing forces evolve. Policy support and affordability are clearly working in favour of apartments, but constrained supply and rising costs are likely to shape the pace and nature of future growth.

What is increasingly clear is that apartments are playing a more central role in Melbourne’s housing market. As population growth continues and affordability pressures intensify, higher-density housing is becoming not just an alternative to detached homes, but a primary solution to the city’s housing needs.

Joel Robinson

Joel Robinson is the Editor in Chief at Apartments.com.au, where he leads the editorial team and oversees the country’s most comprehensive news coverage dedicated to the off the plan property market. With more than a decade of experience in residential real estate journalism, Joel brings deep insight into Australia’s evolving development landscape.

He holds a degree in Business Management with a major in Journalism from Leeds Beckett University in the UK, and has developed a particular expertise in off the plan apartment space. Joel’s editorial lens spans the full lifecycle of a project, from site acquisition and planning approvals through to new launches, construction completions, and final sell-out, delivering trusted, buyer-focused content that supports informed decision-making across the property journey