Profits withering on the vine for Australian grape growers

Grapes are more than just the sweet snacks in the fruit bowl. The Australian grape growing industry is highly dependent on the downstream winemaking industry, with about 89% of production heading that way.

The remaining output is sold as table grapes or dried grapes (e.g. sultanas). The industry is highly volatile due to significant uncertainty surrounding future conditions and its dependence on external variables.

The main issues affecting the industry are water availability and rainfall, activity in the downstream markets and wine producers' use of wine grape contracts. In the five years through 2012-13, industry revenue is expected to decrease by an annualised 11.7% to total $1.06 billion.

The industry is dependent on downstream wine exports, which contribute over 38% of revenue to wine manufacturers each year. The value of the Australian dollar has therefore played a prominent role in the past five years.

Since the global economic downturn, the rapid rise in the value of the Australian dollar has meant that demand for Australian wines has decreased on the global market. This has caused difficulties for wine manufacturers and growers alike.

Moreover, weaker demand for wine in significant export markets such as the United States and the United Kingdom is affecting Australian growers, in the form of lower prices received. As a result, industry revenue is expected to increase by only 2.3% in 2012-13.

The industry has wavered between conditions of over and under supply due to a number of factors, though largely influenced by the huge number of growers and the onset of drought-ridden growing conditions.

Recently, high levels of production caused a glut of wine grapes and put downward pressure on prices. Prices in some spot markets are still below production costs, resulting in some growers making large losses.

The combined effect of volatile production levels and changes in downstream wine manufacturing demand is expected to cause industry revenue to decline by an annualised 1.8% over the five years through 2017-18, to a total of $967.5 million.

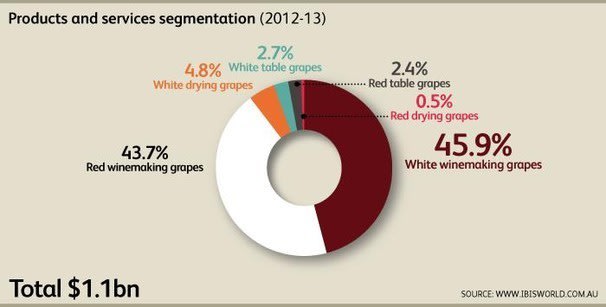

Grape varieties can be broadly categorised as red or white. Furthermore, there are three main uses for grapes: winemaking, drying and eating fresh. Grapes for winemaking dominate the industry.

Red grape varieties account for about 46.6% of the total grape crop, made up of 43.7% wine grapes, 0.5% drying grapes and 2.4% table grapes. There are a number of different varieties of red wine grapes, including shiraz (accounting for 18% of the total grape crop), cabernet sauvignon (12%) and merlot (5.9%). Other prominent red wine grape varieties include pinot noir, ruby cabernet, petit verdot and grenache.

White grape varieties account for 53.4% of the total crop. Again, most grapes grown are wine grape varieties, accounting for 45.9% of the total crop. White drying grapes account for 4.8% of the total crop, while white table grapes account for 2.7%. Prominent white wine varieties include chardonnay (23.9% of total crop), semillon (4.9%), colombard (3.7%) and muscat gordo blanco (2.8%). Sultana grapes account for 6.1% of the total crop, and are used predominantly as drying grapes but also as winemaking and table grapes.

Changes in the relative proportions of red and white grapes in the total crop reflect changes in both planted hectares and yield per hectare. From 2006 to 2007, the area of bearing vines made up of white varieties increased marginally from 40.6% to 41%, with a corresponding decrease in the bearing area of red varieties.

Over the same period, average yields of white varieties dropped from 14.9 tonnes per hectare to 12.1 tonnes per hectare, while average yields of red varieties dropped from 10.9 tonnes per hectare to 7.4 tonnes per hectare. The more prominent drop in red grape yields combined with a decrease in bearing hectares produced a significant fall in red grapes as a proportion of the overall crop.

Industry outlook

Climatic conditions and continued mismatches between demand and supply will affect the performance of the industry in the next five years. Increased demand, along with more balanced supply and demand conditions, will support industry performance over the next five years.

However, it will not be enough to offset the difficult growing conditions, which will primarily drive the projected decline in revenue. Revenue is estimated to decline by an annualised 1.8% over the next five years to reach $967.5 million by 2017-18.

As the global economy shows signs of recovery, demand for wine is expected to strengthen gradually. The limitation will likely be international competition. The abundant supply of wine from many markets around the world is forcing many of these markets to increase their proportion of bulk wine shipments. This will put downward pressure on prices per unit in both domestic and international markets.

If Australian winemakers keep their prices competitive then grape growers' ability to increase their price margin is very limited. Some growers and winemakers are expected to benefit from establishing a strong brand name or niche segment, wherein higher prices can be achieved.

Karen Dobie is general manager of IBISWorld Australia

This article originally appeared on SmartCompany.